You just got your first salary. Or maybe a bonus sitting in your account. Someone told you to invest, but now you are stuck at the very first question: Should you put in a fixed amount every month, or invest everything at once? This confusion around SIP vs lump sum investment in India 2026 is something thousands of beginners go through. In this blog, you will get a clear, jargon-free breakdown so you can stop overthinking and actually start investing.

What Is SIP and How Does It Work?

SIP stands for Systematic Investment Plan. It is a method of investing a fixed amount into a mutual fund every month, automatically. Think of it like a monthly subscription, except instead of spending money, you are growing it.

For example, if you set a SIP of Rs. 1000 per month, that amount gets automatically deducted from your bank account on a fixed date and invested into your chosen mutual fund. You do not need to do anything manually after the initial setup.

Key things to know about SIP:

You can start with as little as Rs. 100 to Rs. 500 per month on most platforms in India

It works on a concept called rupee cost averaging, which means you buy more units when the market is low and fewer units when the market is high

It removes the pressure of timing the market

It builds a consistent savings habit over time

SIP is especially popular among salaried individuals in India because its investment pattern aligns with their monthly income cycle.

What Is a Lump Sum Investment and How Does It Work?

A lump-sum investment means investing a large amount of money in a mutual fund in a single transaction. There is no monthly commitment. You invest once and let the money grow over time.

For example, if you received Rs. 2 lakh as a Diwali bonus and you invest the entire amount into a mutual fund in one go, that is a lump sum investment.

Key things to know about a lump sum:

The minimum investment is usually Rs. 1000 or more, depending on the fund

Returns depend heavily on the market condition at the exact time you invest

If you invest when markets are at a low point, your long-term returns can be very strong

If you invest at a market peak and the market drops shortly after, your entire portfolio takes an immediate hit

It requires more market knowledge and timing judgment compared to SIP

Lump sum investing is best suited for people who already have a large corpus ready to put to work, such as a mature fixed deposit, an inheritance, or a one-time bonus.

SIP vs Lump Sum Investment India 2026: Key Differences

| Factor | SIP | Lump Sum |

|---|---|---|

| Investment Style | Fixed amount every month | One-time large investment |

| Minimum Amount | Rs. 100 to Rs. 500 per month | Usually Rs. 1000 or more |

| Market Timing Required | No | Yes |

| Risk Level | Lower due to rupee cost averaging | Higher |

| Best Suited For | Salaried individuals and beginners | Investors with surplus idle capital |

| Flexibility | High — pause or stop anytime | Less flexible once invested |

| Returns in Bull Market | May be slightly lower | Potentially higher |

| Returns in Volatile Market | More stable | Can fluctuate sharply |

Rupee Cost Averaging: The Biggest Advantage of SIP

One of the strongest reasons beginners are advised to start with SIP is rupee cost averaging. The concept is simpler than it sounds.

When you invest a fixed amount every month, the number of mutual fund units you receive changes based on the current market price. When the market is down, your Rs. 1000 buys more units. When the market is up, your Rs. 1000 buys fewer units.

Over a period of time, this natural averaging means your overall cost per unit tends to be lower compared to investing everything in one go at a single price point. This is why SIP investors are generally less affected by short-term market crashes than lump sum investors.

When Should a Beginner Choose SIP in 2026?

SIP is the right choice for you if:

You have a regular monthly income, such as a salary or freelance payments

You do not currently have a large amount saved up to invest all at once

You want to start small and build your investment portfolio gradually

You feel uncertain about stock market movements and want to reduce your risk exposure

You prefer a hands-off investment approach without monitoring market conditions daily

For most beginners in India, a SIP in Nifty 50 index funds or diversified equity mutual funds is considered one of the most practical and beginner-friendly investment strategies going into 2026.

When Should a Beginner Choose Lump Sum in 2026?

A lump sum can make sense for you if:

You have received a large one-time amount,, such as a bonus, a matured FD, or an inheritance

The market is currently at a relatively low point,, and you have done enough research to feel confident

You have a long investment horizon of at least 5 to 7 years

You are comfortable with short-term volatility and do not panic during market dips

A smart approach for beginners who want to invest a lump sum without taking on too much risk is to use an STP or Systematic Transfer Plan. You park your lump sum in a liquid fund first and then automatically transfer a fixed amount each month into an equity fund. This gives you the discipline of SIP while also putting your money to work from day one.

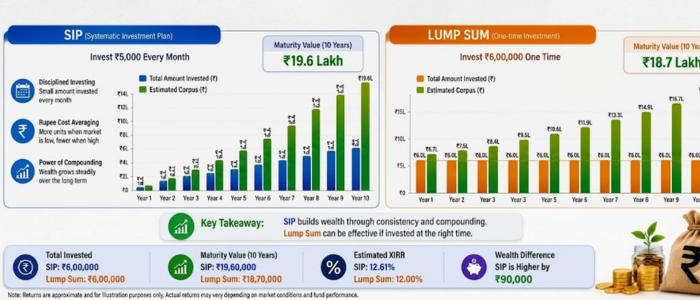

SIP vs Lump Sum: A Realistic Returns Example

Consider two beginners, Rahul and Priya, both investing in a mutual fund with an average annual return of 12 percent.

Rahul starts a SIP of Rs. 5000 per month and stays invested for 10 years.

Priya invests Rs. 60,000 as a lump sum at the start and holds it for 10 years.

After 10 years:

Rahul (SIP): Total invested Rs. 6,00,000. Approximate corpus around Rs. 11,61,000

Priya (Lump Sum): Total invested Rs. 60,000. Approximate corpus around Rs. 1,86,000

The comparison is only fair when total invested amounts are similar. The key takeaway is that SIP builds a significantly larger corpus over time because you keep adding money consistently. Lump sum delivers stronger relative returns when you have a large corpus ready and can time your entry well.

Tax on SIP and Lump Sum Investments in India 2026

Both SIP and lump sum investments in equity mutual funds follow the same capital gains tax rules in India:

Short Term Capital Gains (STCG): If you redeem within 1 year of investment, gains are taxed at 20 percent

Long Term Capital Gains (LTCG): If you redeem after 1 year, gains above Rs. 1.25 lakh in a financial year are taxed at 12.5 percent

For SIP investors, each monthly installment is treated as a separate investment with its own purchase date and holding period. This means units bought in the first month may qualify for LTCG, while units purchased last month would fall under STCG if redeemed today.

For lump sum investors, the entire investment has a single purchase date, making the holding period calculation much simpler to track.

Common Mistakes Beginners Make With SIP and Lump Sum

Stopping SIP during a market fall: This is when SIP works best. Stay invested.

Investing a lump sum at a market peak: No market knowledge? Use STP instead.

Waiting for the perfect time: There is no perfect time. Starting late costs more than starting small.

Picking the wrong fund type: Index funds and large-cap funds are safer for beginners than small-cap or sectoral funds.

SIP vs Lump Sum: Which One Should You Choose in 2026?

The honest answer is this. If you are a beginner with a steady monthly income, start with SIP. It is safer, simpler, requires no market expertise, and forgives early mistakes far more easily than lump sum investing.

If you have received a sudden large amount, do not rush to invest it all at once. Use STP to move it into equity gradually while it earns returns sitting in a liquid fund.

If you are someone who has spent time understanding markets, has a long-term outlook, and can handle short-term volatility without panicking, a lump sum during a market correction can be a very effective wealth-building strategy.

The single most important step is to begin. Not next month. Not after the next market dip. Today.

Conclusion

SIP and lump sum both build wealth; the right choice depends on your situation. If you earn a monthly salary, SIP is the safest and simplest way to start. If you have a large amount ready, use STP to invest it gradually. Neither method works if you keep waiting for the perfect moment. Pick one, start today, and let time and compounding do the rest.

ALSO READ:

- Top 10 SIP Plans in India (2026) – Best SIP Plans for Long-Term Wealth Creation

- How to Grow Your Wealth with SIPs and Mutual Funds

- 10 Best Earning Apps Without Investment in India (2026) – ₹500/Day Apps

- Top Investment Apps in India for Beginners

- Investment for Beginners: How to Start with Mutual Funds or Stock Market in India

Frequently Asked Questions (FAQs)

Q1. What is the difference between SIP and a lump sum investment?

SIP involves investing a fixed amount every month into a mutual fund. A lump sum means investing a large amount all at once. SIP spreads your market risk over time, while a lump sum exposes your entire capital to market conditions at a single point.

Q2. Which is better for beginners, SIP or lump sum?

SIP is generally more suitable for beginners. You can start with as little as Rs. 500 per month; there is no need to track markets daily, and the automated nature of SIP helps build a consistent investing habit from day one.

Q3. Is a lump sum investment risky?

Yes, a lump sum carries a higher risk compared to SIP because your entire investment enters the market at one moment. If the market falls right after you invest, your portfolio is immediately impacted. SIP reduces this risk by spreading investments across multiple market cycles.

Q4. What is the minimum amount required to start a SIP in India?

Most mutual fund platforms in India allow you to start a SIP with Rs. 100 to Rs. 500 per month. Some fund houses offer even lower minimums, making SIP one of the most accessible investment options for new investors.

Q5. Can you invest in both SIP and a lump sum at the same time?

Yes, absolutely. Many investors run a monthly SIP for consistent wealth building and additionally make lump sum investments whenever they receive a bonus or surplus amount. Both can be done in the same fund or across different funds.

Q6. How is tax calculated on SIP investments?

Each SIP installment is treated as a separate investment with its own holding period. Units held for more than 1 year qualify for LTCG tax at 12.5 percent on gains above Rs. 1.25 lakh. Units redeemed within 1 year are taxed at 20 percent as STCG.

Q7. Should you stop your SIP when the market crashes?

No. Stopping a SIP during a market crash is one of the most common and costly mistakes beginners make. A falling market means your monthly SIP is buying more units at lower prices, which improves your average cost and strengthens long-term returns.

Comments (0)

Be the first to comment.