Minimum Credit Score for Personal Loan in India (Complete 2026 Guide)

Applying for a personal loan without knowing the required credit score is one of the most common mistakes borrowers make in India. Banks and NBFCs rely heavily on your credit score to judge your repayment capacity and financial discipline. If your score is too low, your application may be rejected instantly. This detailed guide explains the minimum credit score for personal loan in India, bank-wise requirements, approval chances, and how to improve your score before applying.

What Is a Credit Score in India?

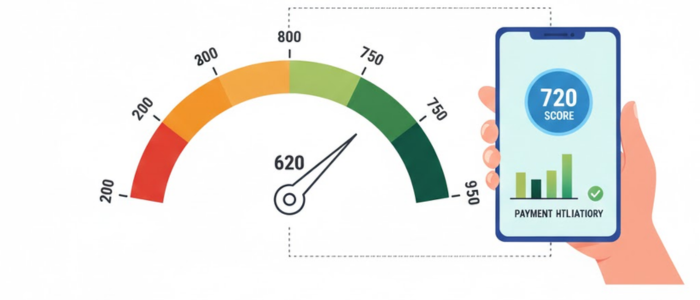

A credit score is a three-digit numerical summary of your credit behavior. It reflects how responsibly you have handled loans and credit cards in the past. In India, lenders primarily consider scores issued by credit bureaus such as CIBIL, Experian, Equifax, and CRIF High Mark, with CIBIL being the most widely accepted.

The credit score range typically lies between 300 and 900:

300–549: Poor – High risk borrower

550–649: Fair – Limited loan options

650–749: Good – Eligible for most loans

750–900: Excellent – Best interest rates and instant approvals

Banks use this score to evaluate loan eligibility, interest rate, loan amount, and repayment tenure.

Minimum Credit Score for Personal Loan in India (Exact Requirement)

The minimum credit score for personal loan in India usually starts from 650. This is considered the baseline score at which many banks begin evaluating an application.

However, approval does not depend on this number alone. Based on industry trends:

650–699: You may get approved, but interest rates can be slightly higher

700–749: Strong approval chances with competitive rates

750+: Fast approvals, higher loan amounts, and lowest interest rates

Applicants with a credit score below 600 generally face rejection from banks and must rely on NBFCs or fintech lenders, often at higher costs.

Bank-Wise Minimum Credit Score Required for Personal Loan

Each bank sets its own internal credit policy. Below is a realistic overview of credit score expectations across major Indian lenders:

Public Sector Banks

Public banks are slightly flexible but strict on documentation.

State Bank of India (SBI): 650+

Punjab National Bank (PNB): ~650

Bank of Baroda: ~650

These banks prefer applicants with stable income and long employment history.

Private Sector Banks

HDFC Bank: 700+

ICICI Bank: 700+

Axis Bank: 700+

Kotak Mahindra Bank: 650–700

Each bank sets its own internal credit policy. You can also check RBI’s guidelines on personal loans for detailed rules and regulations.

NBFCs & Fintech Lenders

- Bajaj Finserv, Tata Capital, EarlySalary: 600–650

NBFCs offer easier approvals but compensate with higher interest rates and processing fees.

Can You Get a Personal Loan with Low Credit Score in India?

Yes, but conditions are tough.

If your credit score is below 650, lenders may:

Reduce loan amount

Increase the interest rate significantly

Shorten loan tenure

Demand a co-applicant or guarantor

In extreme cases, loans are approved only after salary account verification or employer confirmation.

Important Tip:

Avoid applying to multiple lenders with a low score. Every rejection leaves a negative impact on your credit profile.

Difference Between Minimum Eligible and Safe Credit Score

Many borrowers confuse eligibility with safety.

Minimum eligible score: 650

Safe credit score: 700+

Ideal credit score: 750+

A safe score ensures:

Lower interest rates

Higher loan eligibility

Negotiation power

Faster approval

Other Factors Banks Check Apart from Credit Score

While a credit score is the first screening tool, banks never approve a personal loan based on this factor alone. Lenders evaluate your overall financial stability to minimize default risk.

1. Monthly Income

Your income determines whether you can comfortably repay the loan. Most banks require:

₹15,000–₹25,000 minimum salary for metro cities

Higher income for larger loan amounts

Higher income improves loan eligibility even if your credit score is slightly below ideal.

2. Employment Stability

Banks prefer applicants with:

At least 6–12 months in current job

2+ years of total work experience

Frequent job changes may signal instability and increase rejection risk.

3. Debt-to-Income Ratio (DTI)

DTI shows how much of your income goes toward existing EMIs.

Ideal DTI: below 40%

Above 50%: High rejection chances

Lower DTI reassures banks that you can handle additional EMIs.

4. Repayment History

Late payments, loan settlements, and defaults significantly reduce approval chances, even with a good credit score.

5. Employer and City Profile

Employees of reputed companies and residents of metro cities often receive:

Faster approvals

Higher loan limits

Lower interest rates

ALSO READ: Best Loan Apps for Students Without Income in India (2025)

How Credit Score Affects Personal Loan Interest Rates

Your credit score directly determines how expensive your personal loan will be.

Why Interest Rate Depends on Credit Score

A higher credit score indicates lower risk, so banks reward you with:

Lower interest rates

Flexible tenure

Higher loan amounts

Low scores increase perceived risk, leading to higher rates.

Interest Rate Comparison by Credit Score

| Credit Score | Interest Rate Impact |

|---|---|

| 750+ | Lowest rates (10%–12%) |

| 700–749 | Competitive rates (12%–15%) |

| 650–699 | Higher rates (15%–20%) |

| Below 650 | Very high rates or rejection |

Even a 1–2% rate difference can increase total interest by tens of thousands over the loan tenure.

⚠️ Disclaimer: Interest rates mentioned above are indicative and may vary depending on the lender’s policies, applicant profile, income, and market conditions.

How to Improve Credit Score Quickly Before Applying

Improving your credit score is possible with disciplined financial habits. While instant fixes are impossible, meaningful improvement can happen within 3–6 months.

1. Pay All EMIs and Bills on Time

Payment history contributes the most to your credit score. Even one missed payment can hurt your profile.

2. Reduce Credit Card Utilization

Use less than 30% of your credit limit. High utilization signals financial stress.

3. Avoid Multiple Loan Applications

Every loan application creates a hard inquiry, which reduces your score.

4. Clear Pending Dues

Clear old defaults and overdue amounts as soon as possible.

5. Check Credit Report for Errors

Incorrect late payment entries or closed loans showing active can drag your score down. Raise disputes immediately.

Minimum Credit Score for Personal Loan: Salaried vs Self-Employed

Credit score expectations vary based on income stability.

Salaried Individuals

Minimum score: 650

Stable salary and employer reputation matter more.

Salary slips and bank statements are key documents.

Self-Employed Individuals

Preferred score: 700+

Bank's check:

Income consistency

ITR filings (last 2–3 years)

Business stability

Self-employed applicants face stricter evaluation due to income fluctuation.

Common Mistakes That Reduce Credit Score

Many borrowers unknowingly damage their credit score. Avoid these mistakes:

1. Missing EMI or Credit Card Payments

Even a single missed payment stays on your report for years.

2. Making Only Minimum Card Payments

This increases the outstanding balance and interest burden.

3. High Credit Utilization

Maxing out credit cards signals over-dependence on credit.

4. Closing Old Credit Cards

Old cards improve credit history length; closing them can reduce score.

5. Too Many Short-Term Loans

Multiple small loans create a negative impression of credit hunger.

6. Ignoring Credit Report Monitoring

Errors go unnoticed and silently damage your profile.

Conclusion

Understanding the minimum credit score for personal loan in India empowers you to apply strategically and avoid rejection. While a score of 650 may qualify you, maintaining a score above 700 ensures smoother approvals, lower interest rates, and higher loan eligibility. Before applying, review your credit report, correct errors, and strengthen weak areas. A strong credit score is not just a loan requirement, it is a long-term financial advantage.

ALSO READ: Top 5 Cashback Credit Cards for Online Shopping (2025)

FAQs – Minimum Credit Score for Personal Loan in India (People Also Ask)

Q1. What is the minimum credit score required for a personal loan in India?

The minimum credit score required for a personal loan in India is usually 650. However, most banks prefer a score of 700 or above for faster approval and lower interest rates.

Q2. Is 650 a good credit score for a personal loan?

A credit score of 650 is acceptable, but it is not ideal. You may get loan approval, but interest rates can be higher and loan amount may be limited compared to applicants with 700+ scores.

Q3. Can I get a personal loan with a credit score below 600?

Yes, but options are limited. Most banks reject applications below 600, but some NBFCs and fintech lenders may offer loans at higher interest rates and stricter terms.

Q4. What credit score gives instant personal loan approval?

A credit score of 750 or above offers the highest chance of instant approval, better loan limits, and the lowest interest rates.

Q5. Does salary matter more than credit score for personal loan?

Both matter, but credit score is the first eligibility filter. Even with a high salary, a poor credit score can lead to rejection.

Q6. Can first-time borrowers get a personal loan without credit score?

Yes, some banks and NBFCs offer loans to first-time borrowers, but loan amounts are smaller, and approval depends heavily on income and job stability.

Q7. What credit score is required for personal loan in SBI?

SBI generally requires a minimum CIBIL score of 650 for personal loan approval, along with stable income and employment history.

Comments (0)