UPI Cashback Offers 2026: Complete Guide

Every UPI payment you make could be quietly leaving money on the table. Most users stick to one app and miss cashback that other platforms offer for the same transaction. This guide breaks down how UPI cashback actually works in 2026, which apps pay the most, how to stack rewards across layers, and where common mistakes silently cost you money every month.

What Is UPI Cashback and How Does It Work

UPI cashback is a promotional reward that banks, apps, and merchants offer when you complete a payment through the Unified Payments Interface. A portion of your transaction value comes back to you as cash, wallet balance, a scratch card reward, or a voucher. According to the National Payments Corporation of India, UPI transaction volumes have crossed 12 billion a month, and this scale is exactly why banks and fintech apps compete so heavily on cashback to keep users loyal to their platform.

Cashback does not apply automatically to every payment. It usually depends on meeting a condition such as a minimum transaction value, paying a specific merchant, using a linked RuPay credit card, or completing a set number of transactions in a period. Once the condition is met, most apps process the reward instantly, though some campaigns take a few hours to reflect in your account.

According to RBI data, the total value of UPI transactions has crossed ₹18 lakh crore in a single month, which shows just how large the incentive is for apps to keep cashback campaigns running through 2026.

Types of UPI Cashback Offers

Understanding the different reward models helps you pick the right app for the way you actually spend, rather than chasing offers that do not match your habits.

1. Fixed amount cashback: A flat reward once you cross a minimum spend, such as a set rupee amount back on a utility bill above a threshold. Suits users with predictable monthly bills.

2. Percentage-based cashback: A slice of your total bill returned to you, so a higher spend means a higher reward, within the app's daily or monthly cap. Works best for larger, planned purchases.

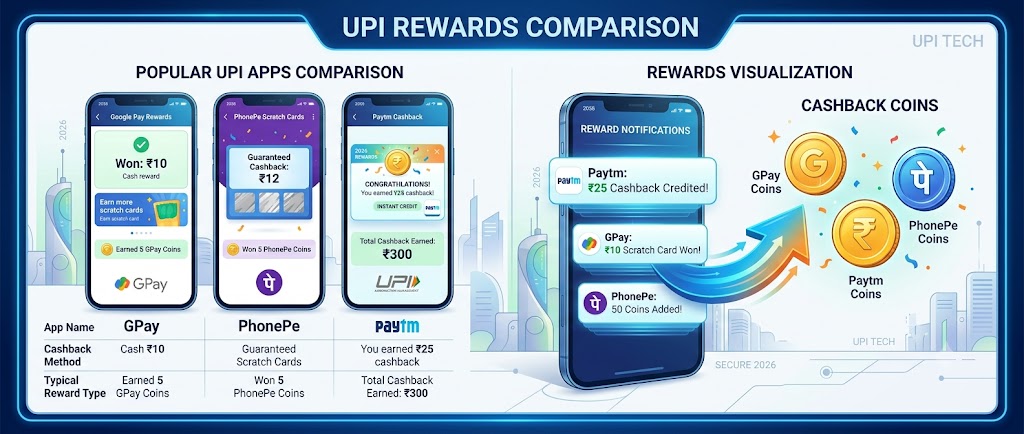

3. Scratch card rewards: Randomised rewards given after a payment, ranging from a small amount to a bigger surprise. Common with apps like Google Pay and keeps engagement high even when average payouts are small.

4. Tiered cashback: Rewards that increase as your transaction count or value grows within a month, favouring frequent users over occasional ones.

Best UPI Apps for Cashback in 2026

No single app wins across every category, so comparing them side by side matters before you pick where to route your daily payments.

| App | Cashback Model | Typical Range | Best For |

|---|---|---|---|

| PhonePe | Campaign driven scratch cards and merchant offers | Varies by campaign | Bill payments, recharges, festival campaigns |

| Google Pay | Scratch cards on eligible payments | Small, randomised | Everyday small transactions |

| Paytm | Wallet credits, promo codes, UPI Lite bonuses | Up to ₹100 on select offers | Recharges and utility bills |

| MobiKwik | Flat percentage on eligible UPI handles, capped per transaction | Up to 5 percent, capped near ₹50 | Aggressive daily cashback hunters |

| Kiwi | Flat cashback via RuPay credit card on UPI | 1.5 percent, up to 5 percent on membership | Users comfortable with credit on UPI |

| slice | Cashback on every scan plus weekly deals | Up to 3 percent | Frequent QR code payments |

| Super.money | Flat percentage cashback, RuPay integration | Up to 5 percent | High reward seekers |

| Tata Neu | NeuCoins on UPI and ecosystem spends | 1 NeuCoin equals ₹1 | Users already inside the Tata ecosystem |

MobiKwik currently runs one of the more visible flat cashback campaigns on regular UPI handles, while Kiwi and slice lean on RuPay credit cards linked to UPI for steadier rewards. PhonePe and Google Pay remain the most widely accepted apps, but their cashback today is more promotional than guaranteed, so checking the offers section inside the app before a large payment is worth the extra minute.

RuPay Credit Card on UPI: A Smarter Cashback Layer

Linking a RuPay credit card to your UPI app adds a second layer of rewards on top of whatever the app itself offers. Most cards in this space return between half a percent and two percent on every scan, and some go higher during specific campaigns. This combination works well for anyone who already pays most merchants through QR codes, since it turns a cashback ceiling into a cashback floor that applies no matter which app you use.

Cards like Kiwi and slice are built specifically around this model, which is why they consistently outperform plain bank linked UPI on high frequency, low value payments like daily groceries, fuel, and food delivery.

How to Claim UPI Cashback Step by Step

Most cashback offers follow a similar claiming process, even though the exact screens differ from app to app.

1. Check the offers section first: Open your UPI app's offers or rewards tab before making the payment, not after, since some offers require activation in advance.

2. Confirm the minimum spend: Note the minimum transaction value or merchant restriction attached to the offer so your payment actually qualifies.

3. Complete the payment as usual: Pay through the UPI PIN flow exactly as you normally would, since most offers apply automatically once the condition is met.

4. Watch for the reward: Cashback usually appears as a scratch card, a wallet credit, or a direct bank credit within minutes, though some campaigns take up to 24 hours.

5. Track larger rewards: Keep a rough note of bigger cashback amounts across the year, especially if you use multiple apps, so you are not caught off guard by the tax threshold later.

UPI Cashback vs Credit Card Rewards

It helps to know how UPI cashback compares to traditional credit card reward points, since many users end up choosing between the two rather than using both.

Traditional credit card rewards are usually points-based, need redemption through a catalogue or statement credit, and often come with annual fees attached to the card. UPI cashback, on the other hand, is typically instant, requires no redemption step, and many UPI apps carry no annual cost at all. The gap narrows when a RuPay credit card is linked to UPI, since that combines a card's reward structure with UPI's instant, no-redemption cashback. For most everyday spending in India, linking a no-fee or low-fee RuPay card to UPI tends to give a simpler and faster reward experience than chasing points on a traditional card.

How to Stack UPI Cashback for Maximum Savings

The biggest mistake most guides make is treating UPI cashback as a single lever. In reality, the smartest savers stack multiple reward layers on the same spend.

1. Layer one: Start with a RuPay credit card linked to UPI for a guaranteed base cashback on every scan.

2. Layer two: Add an app specific campaign on top when one is active, such as a scratch card or festival offer.

3. Layer three: For purchases made through creator storefronts, use a platform that adds its own reward on top. Zokera, for example, gives shoppers follower cashback on qualifying storefront purchases, so a single purchase can combine UPI cashback, a card reward, and a follower cashback credit at the same time.

If you regularly shop through creator recommended stores, checking whether the storefront runs on a platform with 1000+ brand partnerships and its own follower cashback program is a simple way to add a third reward layer without changing how you already pay. Stacking three layers like this across regular shopping, rather than one, is where the real savings show up over a month rather than on a single transaction.

Festival Season Cashback Strategy

Cashback rates typically rise during major shopping seasons like Diwali, and this is when apps push their highest percentage offers and biggest scratch card pools. Planning big ticket purchases, electronics, appliances, or bulk shopping around these windows rather than making them at random points in the year can meaningfully increase how much cashback you collect. Checking the offers section of your primary UPI app and any linked RuPay card a few days before a festival window, rather than on the day itself, helps you catch limited slot campaigns before they run out.

UPI Cashback and Tax: What You Need to Know

Cashback earned through UPI is generally not taxable unless the total across a financial year crosses ₹50,000, based on how promotional rewards are typically treated under Indian tax rules. Beyond that threshold, it may need to be reported as income, so it is worth tracking larger cashback totals if you are an active reward hunter across multiple apps and cards. For anything beyond a general understanding, checking the latest guidance on the Income Tax Department website or consulting a tax professional is the safer route, since treatment can vary based on how the reward is structured and which app issues it.

Common Mistakes That Cost You Cashback

Many users lose out on rewards simply because they are not paying attention to a few details that apps do not always highlight clearly.

Paying below the minimum transaction value required for an offer

Using a personal UPI handle when a campaign is only valid on a specific merchant handle

Ignoring daily or monthly caps and continuing to transact past the point where cashback stops applying

Skipping the in-app offers section before a large payment and missing a live campaign

Splitting bills without checking whether the merchant allows it, which can void an offer rather than double it

Is UPI Cashback Worth the Effort

For occasional, small transactions, cashback adds a small but real saving over time. For anyone making frequent payments, whether through bill pay, recharges, or regular online shopping, the combination of a RuPay card, an active app campaign, and platform-level rewards like Zokera's follower cashback can add up to a noticeable amount across a month. It is less about chasing every scratch card and more about picking two or three reliable layers and using them consistently.

If you found value in this comparison, our Best Online Shopping Sites India 2026 guide covers where these cashback layers stack best across categories, and our piece on digital storefronts for Indian creators explains how follower cashback fits into the wider creator commerce model.

ALSO READ:

- Best Cashback Credit Cards in India 2026

- Top 5 Cashback Credit Cards for Online Shopping

- Minimum Credit Score for Personal Loan in India

- Best Student Loan Apps Without Income in India

- Top 10 Low Interest Personal Loan in India (2026)

- Best Instant Loan Apps in India for Quick Cash

- Top 10 Best Business Loans in India (2026)

Frequently Asked Questions (FAQs)

Q1. Is UPI cashback the same across all banks?

No, cashback depends on the app and card you use, not the bank behind your account.

Q2. Do I need a credit card to get UPI cashback?

No, many apps offer cashback on regular bank-linked UPI payments too.

Q3. Can I use two UPI apps to double cashback on one payment?

No, cashback applies only through the app used to complete that specific transaction.

Q4. Is UPI cashback credited instantly?

Most cashback is instant, though some campaigns take a few hours to a day.

Q5. Does UPI cashback expire?

Wallet-based cashback can expire, while direct bank credit cashback usually does not.

Q6. Is there a limit on UPI cashback per day?

Yes, most apps cap cashback per transaction and per day.

Q7. Can businesses also earn UPI cashback?

Some merchant-specific programs exist, but consumer cashback apps are built for personal payments.

Q8. Does splitting a bill help get more cashback?

It can help only if each split payment separately meets the merchant's minimum cashback threshold.

Q9. Are scratch card rewards guaranteed?

No, scratch cards are randomised and can sometimes return zero reward.

Q10. Is follower cashback different from UPI cashback?

Yes, follower cashback is a platform-level reward on qualifying purchases, separate from what your UPI app offers.

Comments (0)